Aave (AAVE)

Aave (AAVE)

$85.20 -7.44% 24H

- 47Soziale-Stimmungs-Index (SSI)-15.36% (24h)

- #120Marktimpuls-Ranking (MPR)+18

- 1024-St. in Social Media-9.09% (24h)

- 100%24 Std-Bullisch-Verhältnis8 aktive Meinungsbildner

- Zusammenfassung

- Bullische Signale

- Bärische Signale

Soziale-Stimmungs-Index (SSI)

- Daten insgesamt47SSI

- SSI-Trend (7-Tage)Preis (7 Tage)StimmungsverteilungExtrem bullisch (60%)Bullisch (40%)SSI Einblicke

Marktimpuls-Ranking (MPR)

- Warnungseinblick

Beiträge auf X

jfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregabjfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab

jfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregabjfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab 98 5 17.93K Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch

98 5 17.93K Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch- Trend von AAVE nach VeröffentlichungExtrem bullisch

- Trend von AAVE nach VeröffentlichungBullisch

Stani Founder DeFi_Expert C300.57K @StaniKulechov

Stani Founder DeFi_Expert C300.57K @StaniKulechov simo D3.46K @alphaleaked

simo D3.46K @alphaleaked 118 14 13.06K Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch

118 14 13.06K Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch- jfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab

BSCN Media C1.36M @BSCNews228 16 18.23K Original lesen >Trend von AAVE nach VeröffentlichungBullisch

BSCN Media C1.36M @BSCNews228 16 18.23K Original lesen >Trend von AAVE nach VeröffentlichungBullisch - Trend von AAVE nach VeröffentlichungExtrem bullisch

Chris Barrett Media Influencer B19.76K @ChrisBarrett

Chris Barrett Media Influencer B19.76K @ChrisBarrett MSB Intel Media Influencer B39.59K @MSBIntel

MSB Intel Media Influencer B39.59K @MSBIntel

435 7 14.83K Original lesen >Trend von AAVE nach VeröffentlichungBullisch

435 7 14.83K Original lesen >Trend von AAVE nach VeröffentlichungBullisch- Trend von AAVE nach VeröffentlichungBullisch

- Stani Founder DeFi_Expert C300.57K @StaniKulechovjfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab171 20 16.67K Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch

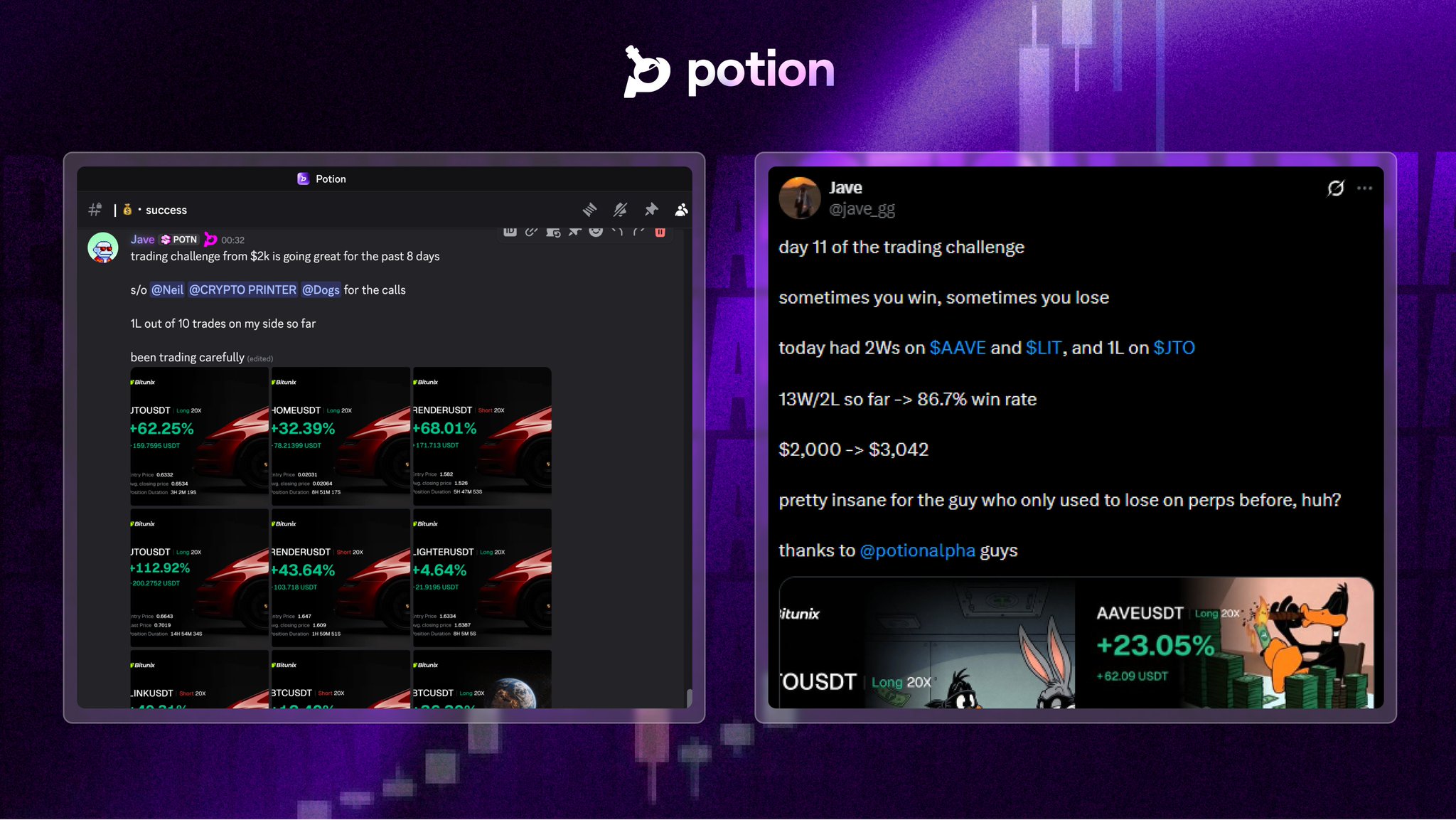

Jave Influencer Community_Lead B6.12K @jave_gg

Jave Influencer Community_Lead B6.12K @jave_gg Potion D58.18K @potionalpha

Potion D58.18K @potionalpha 6 2 330 Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch

6 2 330 Original lesen >Trend von AAVE nach VeröffentlichungExtrem bullisch