🧐What is Circle falling? Does its moat still exist?

First, the result: I think $CRCL is oversold in the short term; if market sentiment causes further overshoot, I would consider buying a portion,

However, I am not confident about holding it long term at this point; more observation may be needed.

Because the fundamentals and moat have clearly undergone huge changes, as I detail below!

Previously I have been researching a question:

What exactly is a company's true moat?

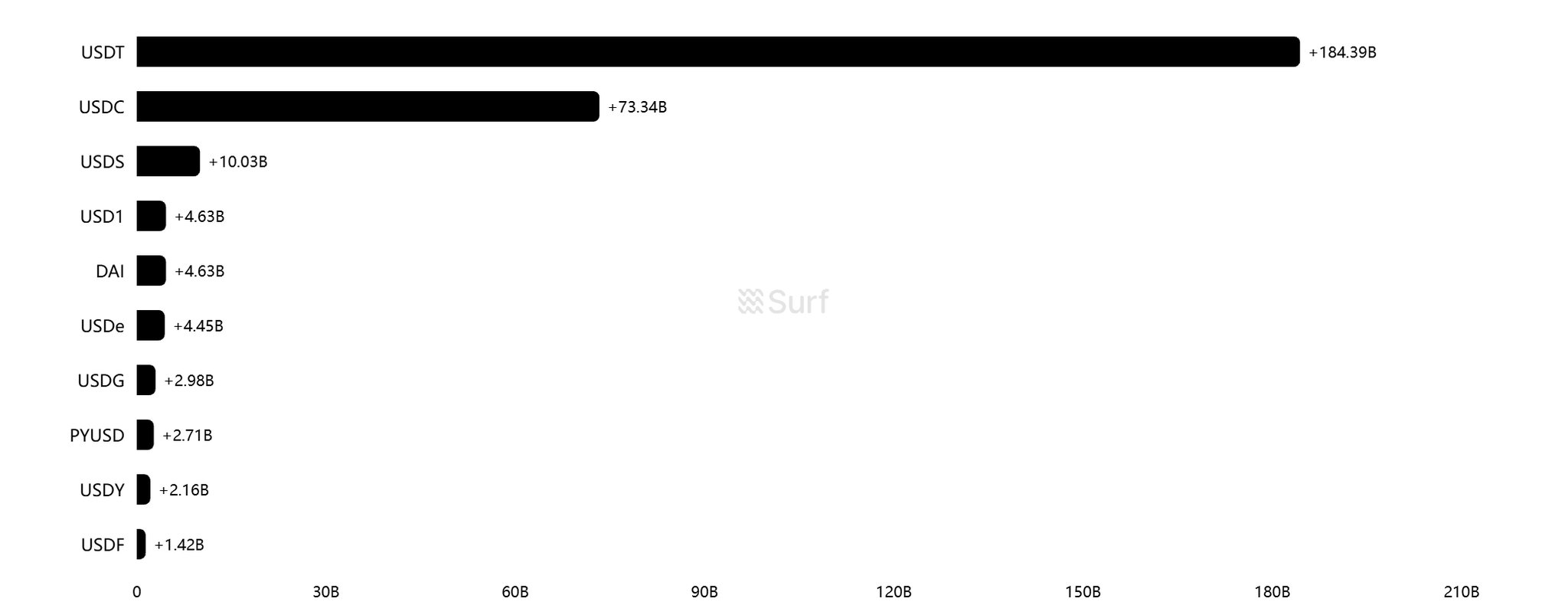

Today, the stablecoin track Open Standard announced the launch of Open USD, a new stablecoin backed by over 140 companies including Visa, Stripe, Mastercard, BlackRock, and Coinbase.

Investors are assessing the competitive threat it may pose to USDC.

The resulting sharp drop provides a very thought‑provoking issue about moats!

1️⃣ What exactly is $CRCL’s decline about?

Open Standard officials also state that Open USD is designed as follows:

Enterprises can mint/redeem at zero cost, with no human‑scale limits; partners receive the reserve asset earnings from Open USD, minus a small management fee; governance is jointly decided by the independent company Open Standard and a partners’ board.

The participant list includes Visa, Stripe, Mastercard, American Express, BlackRock, BNY, Google, Shopify, Coinbase, Solana, Base, Ripple and many other payment, finance, technology and crypto‑infrastructure companies; Stripe also publicly said Open USD will become the default stablecoin choice for Stripe’s business users;

This makes it clear: Open USD is not attacking USDC with technical parameters, but with a distribution mechanism.

Circle’s core profit pool comes from reserve asset earnings; Open USD’s core slogan is to return more of that earnings to the partners that bring traffic.

In other words, OUSD intends to share the economic benefits that were previously retained with Visa, Stripe, Shopify, Coinbase, banks, wallets, exchanges and merchant ecosystems to quickly acquire users.

The “USD 1:1 + on‑chain transfer” technology of stablecoins is not the deepest moat; the real moat lies in trust, regulation, liquidity, distribution, integration, use cases and economic incentives. Now the wolves are coming, naturally people see another possibility.

Therefore I think the representative point here is:

A single technology is not a moat; the ability to continuously turn it into an irreplaceable product and profit for customers is the moat.

I have discussed this theme many times with friends before, why Buffett…