Aave (AAVE)

Aave (AAVE)

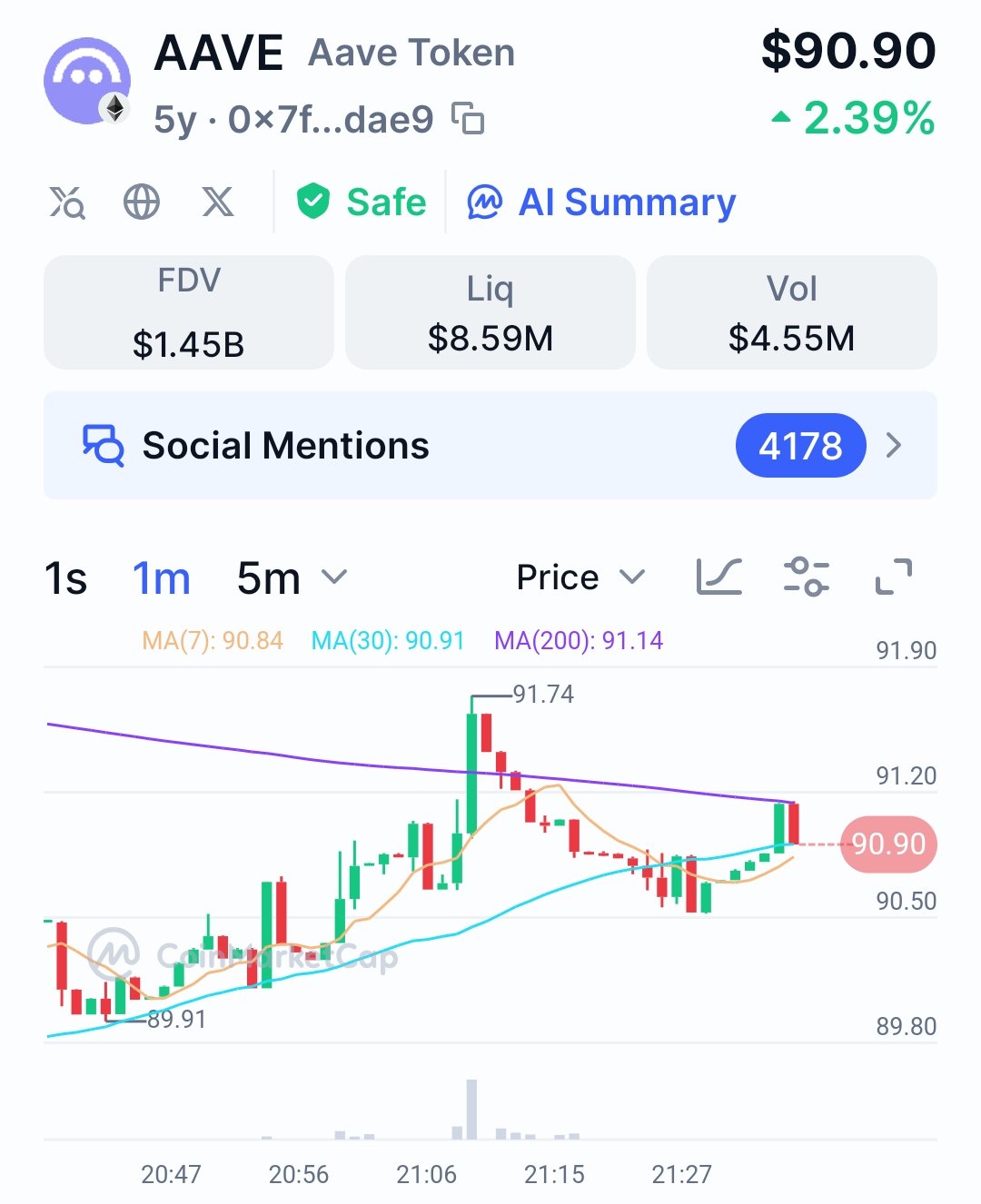

$85.23 -7.41% 24H

- 66Social Sentiment Index (SSI)+48.87% (24h)

- #149Market Pulse Ranking (MPR)-30

- 1424h Social Mention+100.00% (24h)

- 93%24h KOL Bullish Ratio11 Active KOL

- Summary

- Bullish Signals

- Bearish Signals

Social Sentiment Index (SSI)

- Data Overall66SSI

- SSI Trend (7D)Price (7D)Sentiment DistributionExtremely Bullish (36%)Bullish (57%)Neutral (7%)SSI Insights

Market Pulse Ranking (MPR)

- Alert Insight

X Posts

- Trend of AAVE after releaseBullish

- Trend of AAVE after releaseBullish

- Trend of AAVE after releaseExtremely Bullish

Chris Barrett Media Influencer B19.76K @ChrisBarrett

Chris Barrett Media Influencer B19.76K @ChrisBarrett MSB Intel Media Influencer B39.59K @MSBIntel

MSB Intel Media Influencer B39.59K @MSBIntel

404 7 13.48K Original >Trend of AAVE after releaseBullish

404 7 13.48K Original >Trend of AAVE after releaseBullish- Trend of AAVE after releaseBullish

Stani Founder DeFi_Expert C300.57K @StaniKulechov

Stani Founder DeFi_Expert C300.57K @StaniKulechov jfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab

jfab.eth FA_Analyst OnChain_Analyst S9.26K @josefabregab 146 19 14.33K Original >Trend of AAVE after releaseExtremely Bullish

146 19 14.33K Original >Trend of AAVE after releaseExtremely Bullish- Trend of AAVE after releaseExtremely Bullish

Paolo Diomede | Certora Security_Expert Dev B5.12K @pdiomede

Paolo Diomede | Certora Security_Expert Dev B5.12K @pdiomede Mooly Sagiv D2.97K @SagivMooly9 0 1.43K Original >Trend of AAVE after releaseBullish

Mooly Sagiv D2.97K @SagivMooly9 0 1.43K Original >Trend of AAVE after releaseBullish- Paolo Diomede | Certora Security_Expert Dev B5.12K @pdiomede

Certora D11.82K @Certora

Certora D11.82K @Certora 24 1 2.97K Original >Trend of AAVE after releaseBullish

24 1 2.97K Original >Trend of AAVE after releaseBullish - Trend of AAVE after releaseNeutral