We’ve had lots of questions from our investor community looking for thoughts on OUSD, and so I thought I’d share my direct views here for anyone.

Stablecoin networks are platform and network effect businesses that are established over a long period of time, tend towards winner-take-most market structures, and resemble other internet platform utility markets. There are several layers that drive this.

First, stablecoin networks effectively act as public protocols and software layers on the internet and their network strength is a matter of the number and range of applications and services that integrate to the network. Every time a developer or service provider integrates to the network, it brings more network effects. This attracts more developers and adds more utility and more network effects. This then drives demand for the digital currency itself, which then reinforces these network effects through liquidity network effects.

We have realized this at a massive scale with the USDC network today — thousands upon thousands of services integrate with our network, which in turn provides immense utility not just to each application, but to users as a whole who benefit massively from the reach and interoperability that exists. This drives user and developer preference further. We’ve invested in building that ecosystem over nearly a decade, and now it’s accelerating as mainstream institutions come onto the network, connecting their customers and users.

We add to that utility by building software stacks that further expand and strengthen the network — protocols like CCTP and Gateway, which promote interoperability, safety and liquidity around the world. This expands the target surface area for app builders and developers, making it easy for them to tap into the liquidity and network effects that already exist. We are now seeing that stack get pulled into all kinds of chains, permissioned L2s, networks being built by governments, and so much more.

The second layer is that of liquidity network effects. This is fundamental. Liquidity begets liquidity. For a stablecoin to achieve scale and utility, it needs to be highly liquid, both on a primary basis (e.g., through all the major financial market centers in the world, with world class direct banking liquidity) and on a secondary basis both by being available and tradeable for retail and institutional clients in every geography and against every fiat instrument in the world. People who want to access and move value need to be able to easily get in and out of that digital currency. Here, we’ve invested nearly a decade in building out that liquidity, and it is now entrenched in exchanges, DeFI venues, and with PSPs, payments firms, regional exchanges, and so many others. Establishing these liquidity network effects also involves building global regulatory infrastructure and ensuring that the stablecoin is available under various regimes around the world. Today, USDC is in the top 3 most liquid digital assets in the world, and it falls off sharply after that. BTC, USDT and USDC have extraordinary liquidity. The closest other dollar stables are like 10x smaller and that liquidity tends to be concentrated in promotional books in a single exchange, whereas USDC liquidity is dispersed widely across dozens and dozens of surfaces. Building this liquidity has been a nearly decade-long task that we continue.

A third layer of network strength comes from the deep integration with the policy and regulatory environment — in many cases, years of effort to build licensing (e.g., USDC is the only large global stablecoin currently available in all of Europe or Japan), and more regimes for stablecoins are coming online, with Circle leading the way in ensuring that USDC is officially recognized, registered, licensed and accepted in the most important markets in the world. On the back of this is the work of building global banking, reserve management and treasury and liquidity management that can operate this on a nearly 24/7 basis in markets and banking systems globally. This globalization effort is a massive investment that we have made over the years.

All of these investments by Circle and our global ecosystem of thousands of partners have delivered the net result of providing the world’s most trusted and available digital dollar infrastructure—a utility that any user, developer, or business can freely and easily tap into. And we do not intend to slow down.

All of this compounds and shows in the numbers. In Q1 2026, according to third-party analysts (Artemis) who track stablecoin adoption, USDC handled nearly $30T in onchain transactions, representing 80% of all dollar stablecoin transactions on blockchains. USDT handled the remaining 20% of transactions. All of the combined remaining dollar stablecoins handled a total of 0% of transactions (i.e., < 0.5%). While other stablecoins may have some circulation, most of that is through promotions and incentives, the actual usage is extremely limited—because of the extremely limited liquidity and network utility that exists for these coins.

But my thoughts on the competitive landscape are not just about the strength of our network—there are also considerations around any new initiative.

Several perspectives and positioning have been shared about how something like OUSD improves on something like USDC.

1) Free mint and burn. The argument suggests that existing stablecoins charge burn fees, and payments firms should not need to pay these (despite the fact that the entire payment industry is built on small bps fees on various ingress and egress points on their networks). There are structural market realities built around the fact that some stablecoins impose very large redemption fees and have limited redemption facilities – the impact of this is that stablecoins with strong redemption facilities, good liquidity and no fees become the offramp for their competitor stablecoins. It may seem easy to say one will offer unlimited and free redeems, however market reality likely forces other behavior. This can be addressed – and is addressed by Circle – through contractual mechanisms vs. a blanket fee exemption.

2) Everybody wins and shares. While this sounds good in principle, the reality of the market and market opportunity is quite different. Today, Circle shares the majority of its income with its distribution partners, and we continue to lean hard into expanding those partnerships with leading companies across every sector of the market. However, we also retain significant income that allows us to invest in the massive market infrastructure that makes this such a powerful and valuable utility for the world to build on. Giving away all the income is a recipe for starving an infrastructure, systematically underinvesting and ensuring that your platform will remain limited in scope.

Furthermore, Circle believes that the future stablecoin market is likely several orders of magnitude larger than it is today. We’re actively bringing partners into the USDC ecosystem through a diverse and growing set of partnership models that span our work with exchanges, custodians, payments firms, asset issuers and more. We are excited to continue to build with a “big tent mentality” where the entire ecosystem can grow value together.

3) A consortium where everybody has a voice. Perhaps I have a cynical view, but the track record of consortium products achieving scale, P/M Fit or even basic product agility is absolutely dismal, and while there are examples of financial consortia that operate utilities, they are predictably slow moving. Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation and competitiveness. They also typically, out of their own self-interest, starve the consortium itself on an operating basis. We actually tried this in the early days of USDC, and even with a very small group, ran into endless challenges and complexity. Smaller, tighter strategic collaborations and commercial partnership arrangements with product and platform builders that can drive forward independently will almost always outcompete large consortiums. But oftentimes when these get formed, everyone feels like they should put their logo on the list, kiss the ring, and make noise about openness. But typically those same firms will turn to their operating units and make the best decisions for their customers, which often means partnering with the market leader and building durable win-win partnerships.

There’s also been a bunch of commentary on Circle's partnership with Coinbase and what this all means. Our stablecoin partnership with Coinbase remains as strong as ever, and I think we both see that enormous opportunity ahead to expand the USDC network.

A final comment: Circle remains committed to supporting a wide range of different products and infrastructures, even when we might compete with different aspects of those partners’ products in other areas of our business. With OUSD, we work closely with many of the founding members, and we expect that those same members will remain large USDC partners and customers. At the same time, as Circle has diversified our product and platform stack, expanding across Arc, CCTP, CPN, StableFX, Agent Stack and many other areas, we continue to expand the partnerships and collaboration with many other stablecoin issuers — dozens of them — to help them launch on Arc, leverage our interoperability infrastructure, get supported in our Wallets and become settlement and FX options on CPN and StableFX.

We are huge believers in growth in the stablecoin ecosystem and welcome OUSD as a new member of the community!

USDC Dados de preços ao vivo

USDC USDC Histórico de Preços USD

Adquira USDC agora

Compre e venda USDC de forma fácil e segura na BitMart.

Ganhar

Coloque suas criptomoedas ociosas para trabalhar e ganhe renda passiva com poupança, staking e muito mais.

USDC X Insight

181.0K @jerallaire

181.0K @jerallaire  2

2

0

0

723

723

4.5K @Somtum205849

4.5K @Somtum205849 $CRCL good stuff, boss, please keep it.

4.9K @tpsquad_th

4.9K @tpsquad_th Circle in trouble?

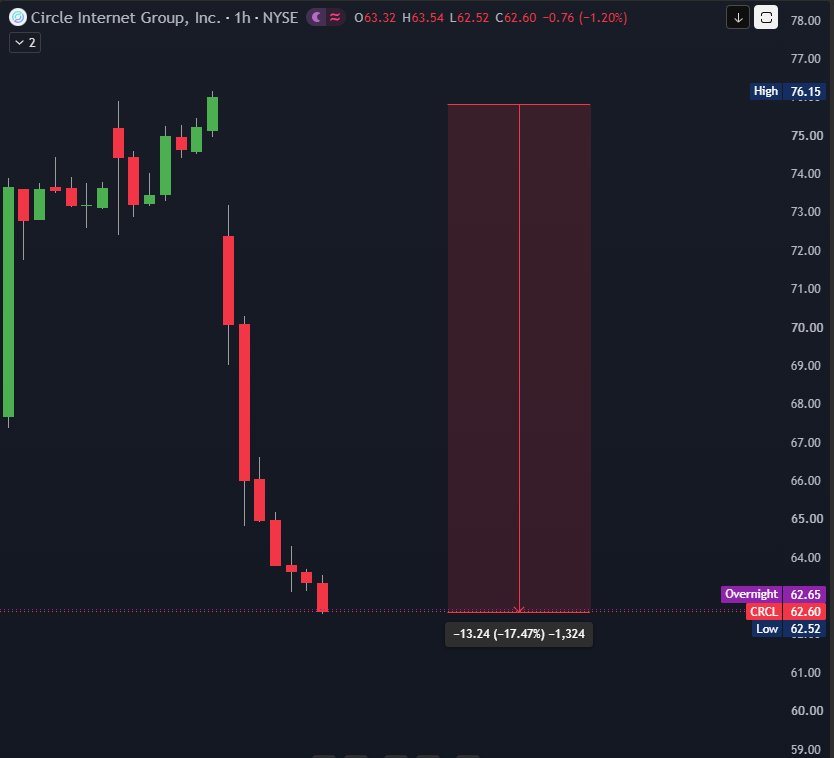

Last night Circle's $CRCL fell more than 17% after the launch of $OUSD.

$OUSD is a new Stablecoin from Open Standard, backed by a consortium of over 140 major companies. Companies that use $OUSD earn interest directly from the Reserve, unlike $USDC which depends on deals.

Major companies include Visa, Mastercard, Stripe, American Express, BlackRock, Coinbase, Google.

Many of these companies were previously partners with Circle.

This launch could significantly affect $USDC's future growth, especially for long‑term partner Coinbase. Even though Circle provides interest from the Reserve held for Coinbase and has recently renewed the partnership, a slowdown in $USDC growth forces Circle to seek deals with other partners and pay them interest, a portion that normally accounts for more than 90% of Circle's profit, resulting in a substantial revenue loss.

On the $USDC side, growth continues to decline, having hit an all‑time high of $79 billion in March 2026 before slipping to $73 billion, roughly comparable to October last year.

Removal from indexes.

In addition, Circle was removed from several Russell Growth indexes during this period.

1

0

165

1

0

165

42.4K @OnchainLens

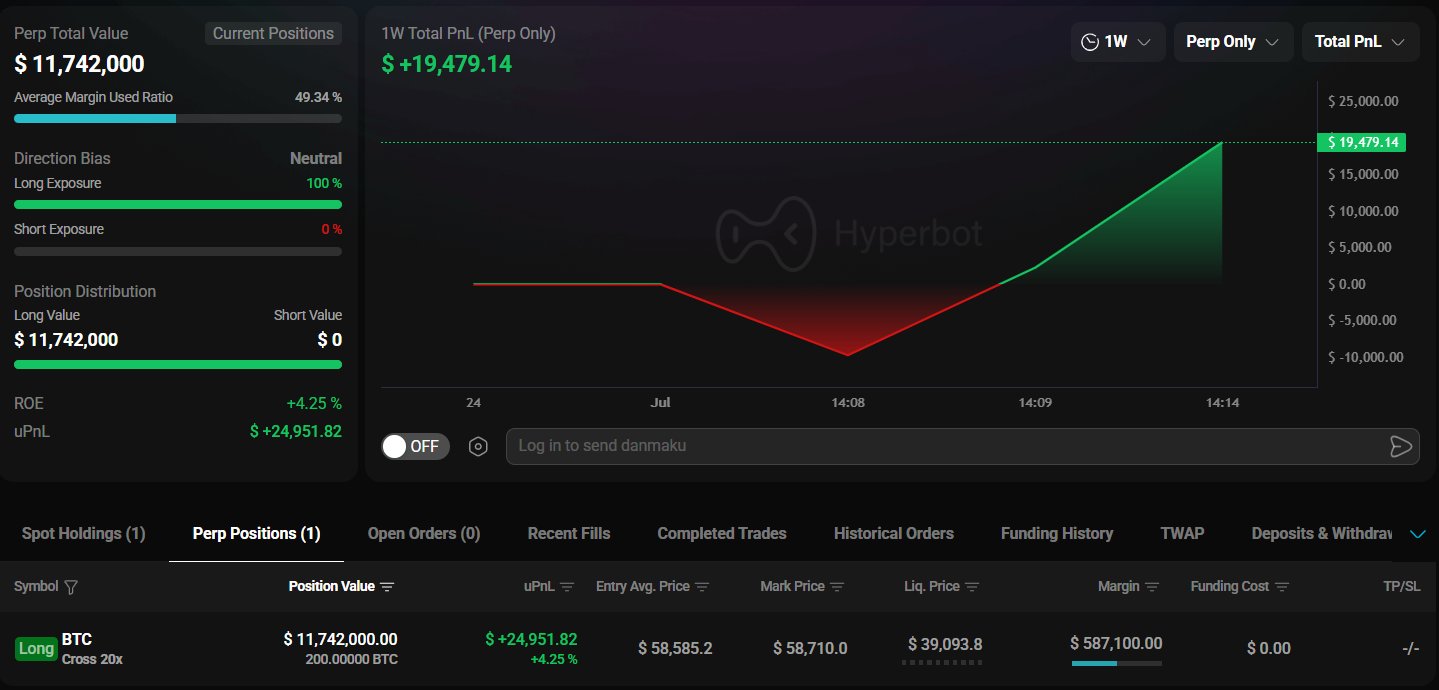

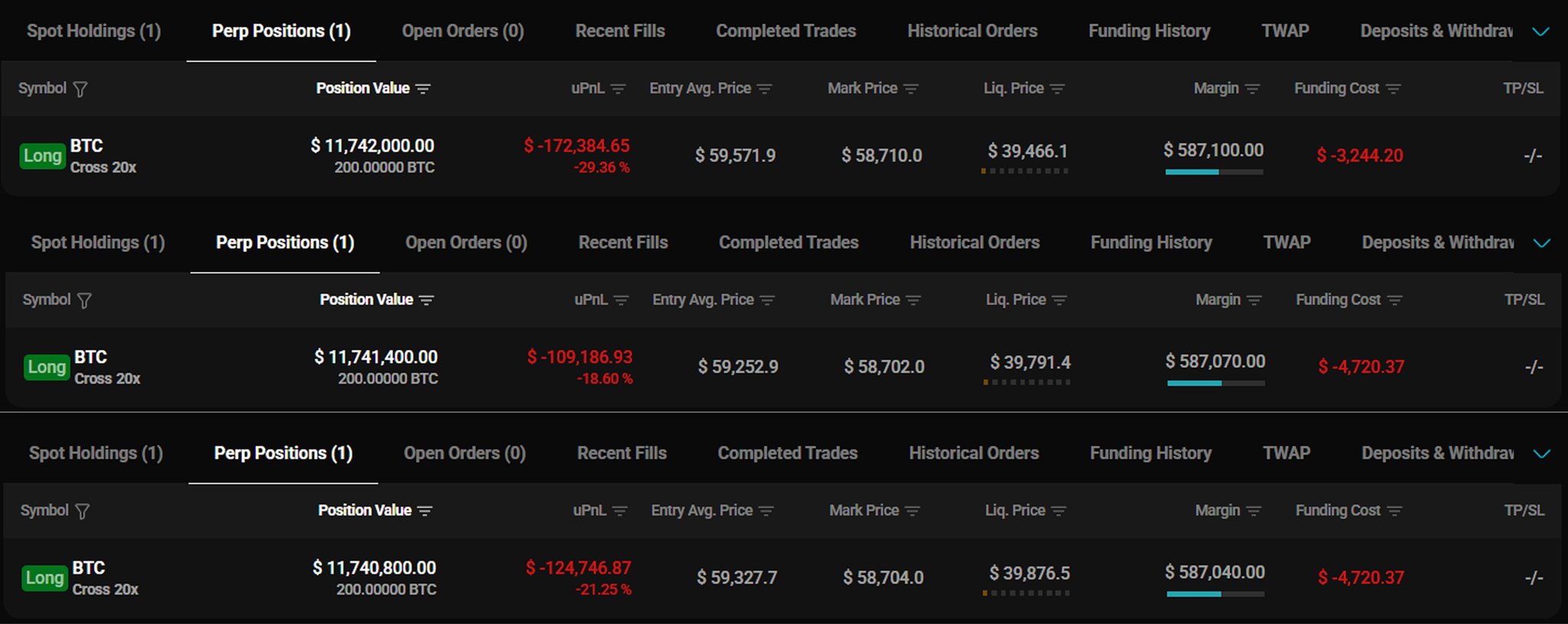

42.4K @OnchainLens A newly created wallet "0x93A" deposit $4M $USDC into #HyperLiquid and opened 200 $BTC long position with 20x leverage

Seems like there are now 4 wallets linked to the same wallets holding 800 $BTC (20x) long position valued at $47M

New Wallet: https://t.co/q48T3e6D3F

Old Wallets:

https://t.co/cVNPBtVC0M

https://t.co/Xdg75nW8Ca

https://t.co/eRIS3tzyfg

10

4

3.2K

10

4

3.2K

Previsão de preço

Quando é um bom momento para comprar USDC? Devo comprar ou vender USDC agora?

Previsão do Beacon

Previsão Probabilística de Preço (Próximas 24 horas)Esta previsão é um produto técnico experimental, fornecida apenas para fins de referência. Ela não constitui uma orientação de investimento. Eventos inesperados no mundo real podem afetar significativamente o comportamento do mercado. Os traders devem tomar decisões com cautela.

USD Coin is a stablecoin brought to customers by Circle and Coinbase. It is an open source, smart contract-based stablecoin. True financial interoperability requires a price stable means of value exchange. CENTRE’s technology for fiat-backed stablecoins brings stability to crypto. The initial implementation is USD Coin (USDC), an ERC-20 token creating possibilities in payments, lending, investing, trading and trade finance — and the ecosystem will grow as other fiat currency tokens are added.

Explore Mais

BM Discovery

Nova Listagem