Отказ от ответственности:

Данные из X (Twitter), собственность оригинальных авторов.Данные приводятся только для справки и не являются инвестиционным советом.

Посты из X

Adrian Morris FA_Analyst Quant S31.51K @_Adrian

Adrian Morris FA_Analyst Quant S31.51K @_Adrian Michael Saylor Founder Influencer C5.07M @saylor0 0 0 Оригинал >Тренд BTC после выпускаБычий

Michael Saylor Founder Influencer C5.07M @saylor0 0 0 Оригинал >Тренд BTC после выпускаБычий- Тренд BTC после выпускаЧрезвычайно бычий

- Тренд BTC после выпускаНейтрально

Milk Road Influencer Educator D101.37K @MilkRoadMilk Road Influencer Educator D101.37K @MilkRoad61 2 21.48K Оригинал >Тренд BTC после выпускаБычий

Milk Road Influencer Educator D101.37K @MilkRoadMilk Road Influencer Educator D101.37K @MilkRoad61 2 21.48K Оригинал >Тренд BTC после выпускаБычий 🇬🇧 ChartNerd 📊 TA_Analyst OnChain_Analyst A34.11K @ChartNerdTA

🇬🇧 ChartNerd 📊 TA_Analyst OnChain_Analyst A34.11K @ChartNerdTA

Diana D23.79K @InvestWithD1 0 688 Оригинал >Тренд XRP после выпускаЧрезвычайно бычий

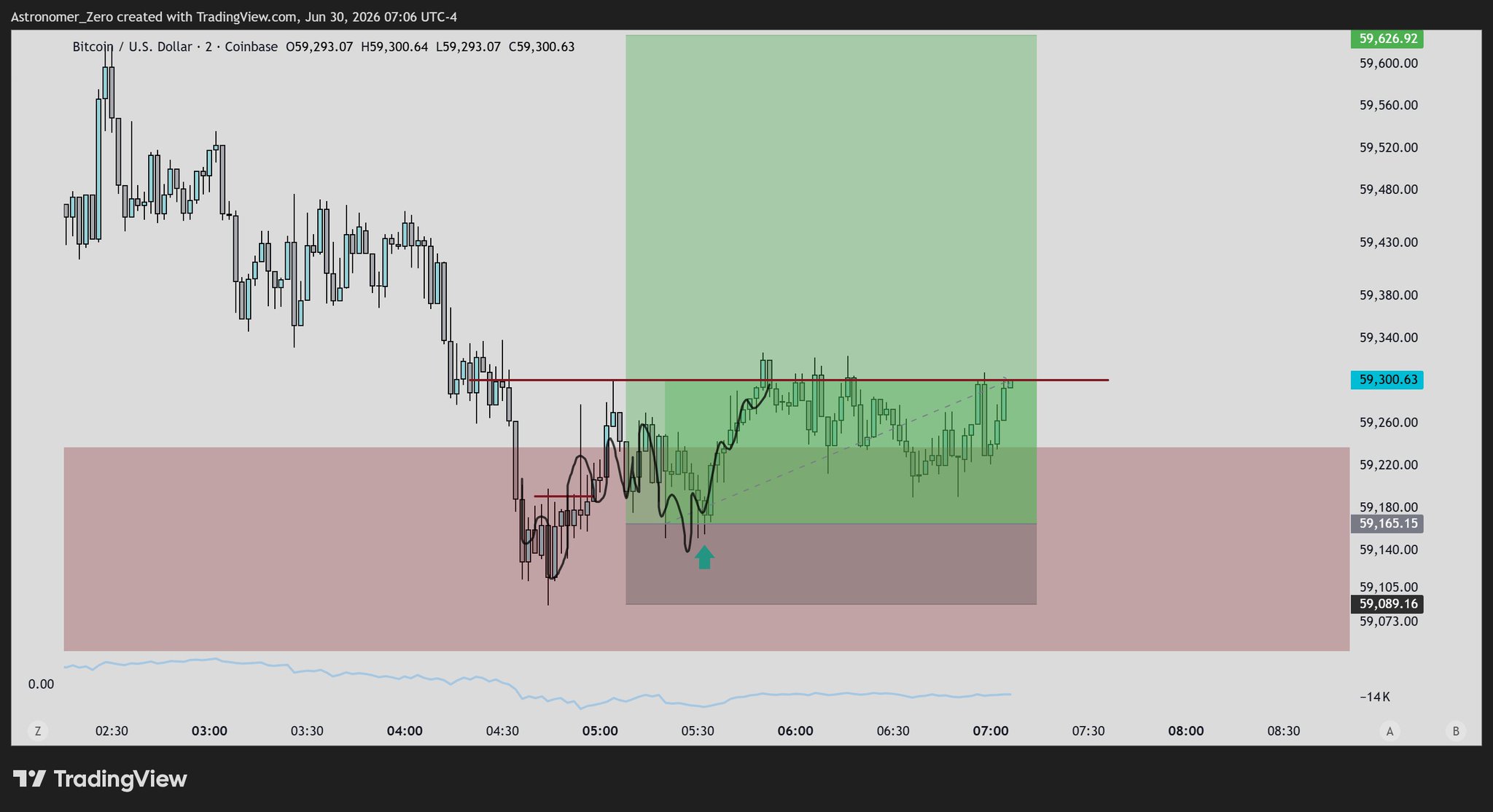

Diana D23.79K @InvestWithD1 0 688 Оригинал >Тренд XRP после выпускаЧрезвычайно бычий Astronomer Trader TA_Analyst S62.16K @astronomer_zero

Astronomer Trader TA_Analyst S62.16K @astronomer_zero Astronomer Trader TA_Analyst S62.16K @astronomer_zero

Astronomer Trader TA_Analyst S62.16K @astronomer_zero 10 2 4.22K Оригинал >Тренд BTC после выпускаБычий

10 2 4.22K Оригинал >Тренд BTC после выпускаБычий- Нейтрально

- Тренд BTC после выпускаБычий

palpal|PalAcademy FA_Analyst Regulatory_Expert B30.42K @palpalNFTpalpal|PalAcademy FA_Analyst Regulatory_Expert B30.42K @palpalNFT

palpal|PalAcademy FA_Analyst Regulatory_Expert B30.42K @palpalNFTpalpal|PalAcademy FA_Analyst Regulatory_Expert B30.42K @palpalNFT 41 2 10.02K Оригинал >Тренд BTC после выпускаНейтрально

41 2 10.02K Оригинал >Тренд BTC после выпускаНейтрально CW OnChain_Analyst Trader B22.77K @CW8900

CW OnChain_Analyst Trader B22.77K @CW8900 CW OnChain_Analyst Trader B22.77K @CW8900

CW OnChain_Analyst Trader B22.77K @CW8900 0 0 0 Оригинал >Тренд BTC после выпускаЧрезвычайно бычий

0 0 0 Оригинал >Тренд BTC после выпускаЧрезвычайно бычий

24-часовой социальный настрой от X

6,640Проанализированные посты+53.49%2,317Опрошенные лидеры мнений+0.04%Рыночные настроения склоняются Бычий- МонетыSSIИзменитьSSI Инсайты

- МонетыMPRИзменить

USUAL#1 Social mentions surged-

USUAL#1 Social mentions surged- LDO#2 Social mentions surge-

LDO#2 Social mentions surge- NEO#3 Social mentions surged-

NEO#3 Social mentions surged- O#4 Social mentions surged-

O#4 Social mentions surged- KAIO#5 Social mentions surged-

KAIO#5 Social mentions surged-

Сводка оповещения